This article explores how structure, not insight, is the bottleneck in credit risk response. Based on a live simulation, it reveals where delay occurs, and how O2C teams can act faster.

Pressure creates clarity.

The signs tend to arrive quietly. A trusted collector misses targets. A regional leader departs without explanation. A change in legislation slips past unnoticed. The tone of a payment conversation shifts from direct to vague. None of this is difficult to spot, particularly for teams with the right experience, a strong network, and a habit of asking the next question. Yet in many cases, the decision to act still comes too late.

Corporate insolvencies are rising again across Europe.

This reversion in the credit cycle has not caught risk professionals unprepared. Most teams now track a blend of financial and behavioural signals. The difficulty lies elsewhere. In many organisations, there is no shared protocol for interpreting ambiguity, no ownership of escalation, and no agreement on when ‘early’ is early enough.

The constraint is no longer insight. It is structure.

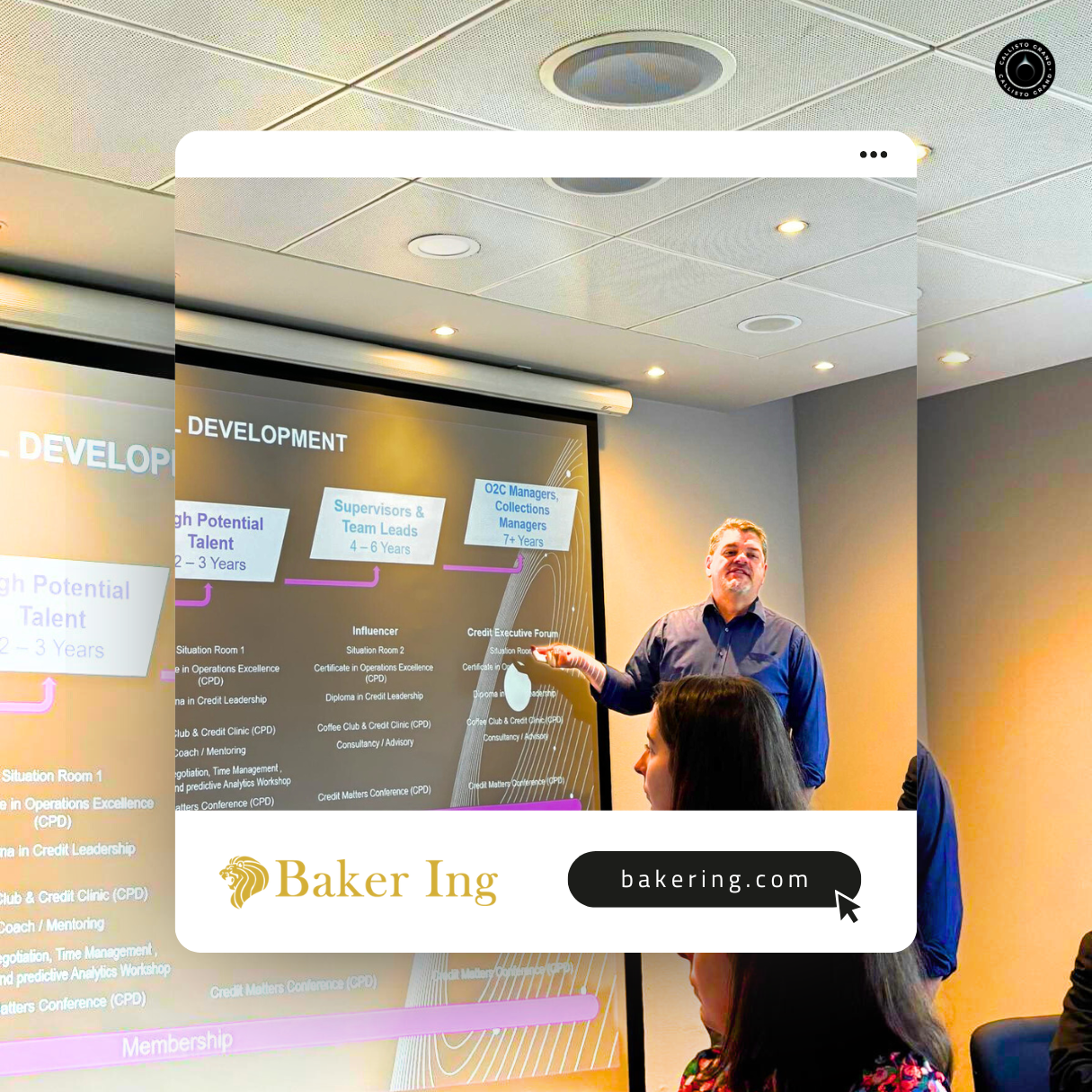

To explore that tension, Baker Ing and Callisto Grand convened a group of 27 Order-to-Cash professionals for a one-day simulation in Birmingham.

The Situation Room format placed delegates in cross-functional leadership teams and asked them to respond to a series of seven real-world case studies. Each table worked through three. Some focused on credit events – missed payments, disputed deductions, deteriorating payer behaviour. Others surfaced broader operational risks, from team performance to strategic blind spots. Each case was grounded in a real scenario. Each required a decision.

Decisions were required. But so was alignment.

The screen displayed a single slide: three tables, grouped as cross-functional leadership teams. Finance, credit, sales and service leads sat side by side, each with a set of case studies in front of them. Alongside those case files, delegates also previewed agentic-AI collection tools and other next-wave O2C automations, debating how much faster promise-to-pay follow-up could become.

Every group was asked to respond to three out of seven real-world scenarios. Some centred on credit-specific issues: a missed payment under review, a growing dispute backlog, a long-standing payer beginning to stall. Others raised broader leadership challenges: underperformance within the collections team, deteriorating morale, and uncertainty around regional oversight. The cases were drawn from real incidents and deliberately stripped of perfect clarity.

The format imposed time pressure from the start. Teams were given a fixed window to read, discuss, and prepare a recommended course of action. There was no perfect answer. But there was a clear expectation: a decision had to be made.

The materials were sparse but sharp. Board packs were anonymised, financial indicators unstable, and narrative cues – some direct, some oblique – forced teams to read between the lines.

-

A collector’s numbers slipping month-on-month

-

A regulatory notice published but not escalated

-

A senior departure with no official communication

There was no room to defer. Once time was called, the group moved on – whether or not internal consensus had been reached.

It became clear early on that the exercise wasn’t testing policy knowledge. It was stress-testing governance. With the same inputs in front of them, what separated one group from another wasn’t who understood the issue first – but who was ready to act, and who was still waiting for alignment.

Why insolvency now demands earlier decisions vs. consensus.

In the third quarter of 2024, compulsory liquidations in the United Kingdom rose by 14 per cent compared with the previous year. Polish insolvency filings climbed by 21 per cent. Ireland saw a 54 per cent increase in new company registrations, interpreted by most credit professionals not as entrepreneurial enthusiasm, but as a fresh wave of phoenix activity.

These are not statistical anomalies. Construction, hospitality and retail – industries structurally exposed to lagging payments and fragile working-capital cycles – are absorbing the pressure first. Several more sectors are likely to follow.

The implication for the day’s participants was unambiguous. Credit models grounded in financial ratios (leverage, interest cover, current ratio) are too slow to capture what practitioners increasingly experience in real time. Liquidity now disappears in days, not quarters. What matters more is the ability to respond to signals that emerge earlier, even if they sit outside the traditional toolkit. Yet few executive dashboards track decision-to-action speed, so early wins often stay invisible.

It was proposed to examine credit through an alternative lens.

-

Track changes in payment patterns.

-

Monitor the exit of key financial decision-makers.

-

Watch for shifts in subsidiary structure or legal status.

Discussion also surfaced classic stakeholder push-back: sales resist credit holds, legal ask for tighter proof, and finance keep an eye on covenant limits…all under severe time pressure.

What surfaced in the gaps between recognition and response.

The early rounds of The Situation Room were not particularly complex. During the debrief, participants flagged deduction-dispute backlogs as a prime example of how unclear ownership keeps cash tied up. The data sets were intelligible, the options were bounded, and the tools available to participants were familiar. Yet the pace of the simulation exposed a set of deeply familiar frictions.

Three themes emerged consistently in the group discussion that followed.

First, ambiguity proved easier to spot than to resolve: Participants broadly accepted that risk indicators were visible early. The difficulty was in translating early signals into action. Finance and sales do not always agree on thresholds. Legal departments often ask for confirmation that never comes. We might discuss the phrasing of a risk advisory while another group move to restrict terms with little delay. The simulation made visible what often remains unspoken in day-to-day practice: caution is rarely about data. It is about permission.

Second, governance structure shaped response time: Where teams agree escalation rules in advance, two indicators and a review proceeds, response time shortened noticeably. Other groups reverted to real-world habits: internal alignment first, stakeholder reassurance second, action third. Several admitted to spending more time preparing communications than executing decisions. This form of delay, whilst routine in many organisations, became stark as a cost when the clock advanced and the options narrowed.

Third, structural dependency on individuals remains an operational blind spot. One scenario required teams to adjust for the sudden absence of a key collector. In most cases, dispute resolution slowed immediately. Participants recognised the problem instantly. A few had a solution ready – the exercise highlighted the leadership cost of knowledge that lives only in heads, not hand-over docs.

As one delegate noted after the event:

“No black-and-white answers, exactly what real life feels like.”

The day did not hinge on theory. It focused on execution.

When participants knew what to do but lacked the consensus or governance to proceed, the simulation moved on regardless. In that space between awareness and action, the real cost of delay became visible and measurable.

Structures, not systems, are now the limiting factor in credit response.

The Situation Room may have been a simulation, but the discomfort it created felt familiar. By the final round, participants were no longer discussing risk in the abstract. They were responding to it, under time constraints, without perfect information, and in view of their peers.

And the final task of the day was deliberately unpolished.

Each delegate was asked to write down a single action they intended to take back into their business. The resulting notes offered a more useful snapshot than any formal review. When pressure removed the usual buffers of hierarchy and process, five priorities stood out across the room:

First, codify the escalation trigger…

Several teams proposed adopting a simple rule: if one financial and one behavioural indicator emerge at the same time (a missed payment and a sudden leadership exit, for instance) a credit review begins automatically. No additional meetings. No further escalation required. The principle was not about being reactive, but about clarifying the point at which action becomes obligatory.

Second, bring behavioural signals into monthly packs…

Participants described current dashboards as skewed towards financial history. Most committed to introducing forward-looking alerts, such as court filings, payment jitter, and director resignations, alongside standard DSO and ageing reports. These signals are rarely definitive, but they often arrive earlier than the more comfortable metrics.

Third, formalise succession in the collections team…

The attrition scenario highlighted how much critical account knowledge sits with individuals. Delegates agreed that naming a secondary contact and maintaining up-to-date handover notes was no longer optional. This was particularly true for cross-border ledgers, where legal familiarity and language skills cannot be replaced at short notice.

Fourth, finalise recovery and legal support terms before they are needed…

A number of teams were caught between urgency and procurement friction. The consensus that followed was straightforward: fee schedules and partner agreements should be signed in advance. Delay does not begin with the debtor, it begins internally, when execution depends on terms still under negotiation.

Fifth, measure decision-speed, not just outcomes…

Several participants acknowledged they had never tracked the time between a first credible warning and the intervention that followed. The commitment, post-event, was to build that measure into governance reporting. The rationale was simple: speed is an operational variable, and should be treated accordingly.

These are modest but practical responses to structural blockers that had been exposed in plain sight. Each action can be implemented without new systems or additional headcount. What was required was clarity, and the shared context that the simulation had provided.

From Simulation to Strategy.

Before leaving, delegates swapped practical playbooks and received concise vendor briefs on next-generation O2C tools they could pilot internally.

Baker Ing and Callisto Grand thank the 27 O2C leaders who stepped into The Situation Room to test their judgement, challenge assumptions, and work through live pressure decisions as a team. The simulation wasn’t about knowledge-sharing. It was about execution: navigating incomplete information, internal tension, and tight timeframes to make real calls that mirror the boardroom.

What emerged was not a lesson in analytics, but in structure. All teams saw the signals. The difference was not insight, but alignment, ownership, and the right to act. That’s the friction the simulation was built to surface. And that’s where real cost lives in modern credit governance.

For Baker Ing, this reinforces a core part of our operating model: we don’t just help clients recover funds, we help them avoid the administrative delays that let risk grow unchecked. Whether acting as recovery partner or pre-emptive advisor, our focus is the same: fast insight, clear authority, precise execution.

If you want to go deeper, you have two opportunities coming up…

Transform O2C: An invite-only working forum for senior O2C and finance leaders who want to reshape decision speed, automation, AI and governance at structural level.

Apply to join at transformo2c.com

Credit Matters Conference: Callisto’s flagship pan-European CPD-accredited conference, combining real-world case studies, strategic panels, practitioner-led workshops, and formal networking.

Register now at callistogrand.com/events/o2cconference