Please notify me of updates:

Watch Real Talk Economics: Here

The road ahead for UK businesses just got trickier.

The Spring Statement 2025 delivered some important updates: growth forecasts were lowered, and inflation projections surged to 3.2%.

In this blog, Markus Kuger, Chief Economic Advisor at Baker Ing, breaks down:

↯ The economic shifts businesses need to prepare for

↯ The sharp rise in debt placements (+82% YoY)

↯ What this means for credit risk in 2025

With inflation staying sticky and interest rates remaining high, the challenges are becoming clear…

Developments

On 27th March 2025, Rachel Reeves, the Chancellor of the Exchequer delivered her Spring Statement, announcing several policy changes that will impact the British economy over the next quarters and years. Positively, businesses were not targeted directly as most measures will impact welfare changes, overseas aid and defence spending as well as new fiscal spending rules.

However, indirectly, the Spring Statement contains several new challenges for Britain’s businesses, especially as it includes a new set of macroeconomic forecasts. While the Office for Budget Responsibility (a public body, created in 2010 and funded by the UK Treasury) has increased growth forecasts for the 2026 to 2029 period, it has slashed the 2025-projection from 2% to now only 1%. At the same time, the OBR’s 2025 inflation forecast moved higher: from 2.6% to now 3.2%, thereby severely exceeding the Bank of England’s 2.0% inflation target.

Lower social welfare spending (aimed at bringing the fiscal deficit under control), coupled with already subdued consumer confidence is likely to adversely impact household consumption. This will be another setback for the UK’s B2C sector, at least temporarily.

Also problematic is the fact that these changes come on the back of the much more substantial Autumn Budget. Back in October, Reeve announced an almost 7% increase in the minimum wage, higher employer national insurance contributions (from 13.8% to 15.0%) and lower national insurance thresholds. As a consequence, companies will experience higher wage costs from April onwards (when these changes come into effect). Simultaneously, UK businesses will be adversely affected by increases in the packaging tax and the government’s flagship Employment Rights Bill (which will increase workers’ rights).

Taking all factors into account, companies’ input costs are set for a sizeable increase., Even without the government-mandated rise of the minimum wage, real regular earnings were rising by a very high 2.1% year on year (y/y) in the three months to January 2025, according to data from the Office for National Statistics (ONS).

Credit Risk

The outlook for credit risk in the UK remains elevated in 2025 due to a combination of factors:

- Sticky inflation will likely reduce the Bank of England’s room to cut interest rates. This keeps borrowing costs high for companies, particularly SMEs.

- Interest rates have fallen since mid-2024 but remain significantly above pre-crisis levels. In February 2025, the effective interest rate on new loans was 6.2%, up from 2-3% in 2010-22.

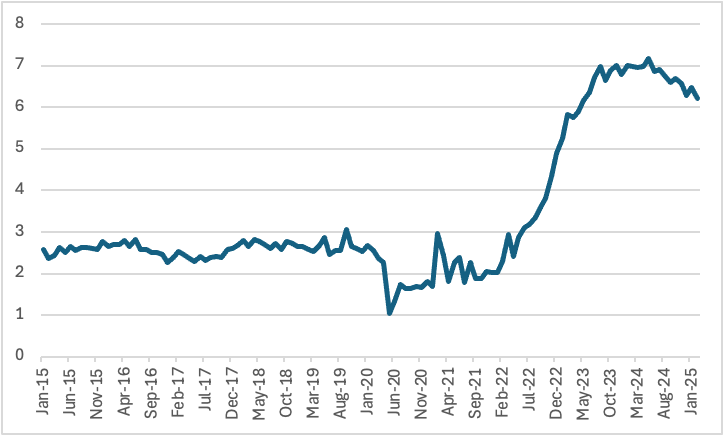

Chart: Effective Interest Rate On New Loans From Banks To UK Private Non-Financial Companies (in %)

Private non-financial companies in the UK were facing an effective interest rate on new loans of 6.2% in February, according to the BoE. While that is down from 7.0% one year earlier, it is up against the levels of 2%-3% seen in 2010-22.

Meanwhile lending to the UK corporate sector has continued to grow in y/y terms in early 2025 (+3.5% y/y in February) but this is driven by large corporations (up by 4%). Lending to SMEs continues to fall (down by 1.4%), a trend that has started in September 2021). Furthermore, lending terms have also tightened substantially, according to the BoE’s Bank Lending Surveys, resulting in an elevated level of credit risk.

Positively, the number of company insolvencies in England and Wales has fallen by around 5% in 2024. That said, the 2024-figure (23,879 business failures) compares unfavourably against the pre-Covid average (2016-19) of 15,615 insolvencies per year. When measured as a share of active companies, the ratio also looks worryingly high: in 2024, there were 52.5 company insolvencies per 10,000 companies, according to data for the government’s Insolvency Service. This is down from the 57.2 recorded in 2023 but up from the 2016-19 average (44.7 per 10,000 active businesses).

Baker Ing ’s data highlights ongoing B2B payment issues in the UK. Baker Ing has seen sizeable growth in the total number of UK debts placed with us (up by 82% in 2024) as well as the pound value of UK debts placed (+54%). At the same time, debts collected in the UK (+11%) have also risen, illustrating a growing demand for debt recovery services in a more challenging financial environment.

As input costs rise, lending terms tighten, and interest rates stay elevated, the likelihood of further credit risk remains substantial in 2025.

About the Author

Markus Kuger is Chief Economic Advisor at Baker Ing , where he leads the company’s economic analysis and strategic insights. With years of experience in macroeconomics and credit risk, Markus provides valuable guidance to businesses navigating the complexities of today’s financial landscape. He is responsible for interpreting key economic trends and advising clients on the implications of market shifts, helping them make informed decisions.

Real Talk Economics

Hosted by Markus, the “Real Talk Economics” series offers a monthly in-depth look at global trade credit trends and economic developments. Through LinkedIn Live sessions and on-demand recordings, Markus provides insights to help businesses navigate the complexities of global trade. Missed a session? Catch up on past episodes and stay informed about upcoming discussions by visiting the Real Talk Economics page.